UK Altnets could increase take-up by revising their go-to-market strategy and adopting proven and successful strategies from similar players in Europe

The fixed broadband market landscape in the UK has been highly competitive but primarily controlled by large nationwide operators such as BT, Virgin Media O2, Talk Talk and Sky.

Subscriber take-up rates for AltNets have been lower than expected despite considerable investments in infrastructure to extend their network reach.

To counter this situation, we believe small AltNets should replicate successful initiatives found in other markets, namely:

- Complement current sales channels with door-to-door and high street presence, specifically in suburban and rural areas where face-to-face is a critical sale point.

- Simple 3P and 4P packages with attractive pricing, bundling AltNets’ traditional broadband with services such as mobile and content, increasing ARPUs and client stickiness.

The prevailing approach among UK AltNets has been digital-centric sales channels.

We are starting to see the first signs of change as OGI, a UK-based AltNet, is pioneering this transition by partnering with Get Connected2 to sell broadband services in physical retail outlets.

This could mark the beginning of an evolution in the UK AltNet landscape to gain a larger market share.

Add sales channel based on door-to-door and high street presence

UK AltNets have primarily relied on digital-centric sales channels reinforced by social media campaigns, word of mouth and telemarketing. However, this model has not proven very effective.

This has been recognised by the main operators, which never abandoned their network of physical stores entirely.

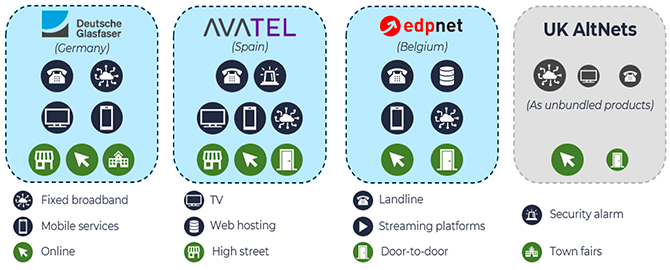

AltNets in European countries have successfully implemented this door-to-door and high-street presence model, typically achieving 25-50% take-up rates, some reaching up to 80%. Notable examples include FiNetwork and Avatel in Spain, EDPnet in Belgium, Deutsche Glasfaser in Germany, and Intred in Italy.

In contrast, UK AltNets average 19% subscriber take-up, and many do not even achieve 10%.

OGI’s addition of a physical sales channel aims to bridge this take-up gap and align better with consumer behaviour across different demographics.

Diversity in product offering and sales channels of selected European AltNets

Simple 3P and 4P packages with attractive pricing

UK AltNets have generally offered stand-alone fixed broadband, leaving customers to seek other providers for mobile communications, fixed voice and other services.

Some AltNets provide fixed voice, TV or streaming platforms as add-on services rather than in bundles.

On the other hand, nationwide fixed broadband providers have leveraged their mobile infrastructure and access to content to provide bundles as their primary offer, which has helped them maximise subscriber retention and ARPUs.

In several European countries, AltNets have successfully combined fixed broadband with other services.

They have used neutral platforms for MVNOs and content and strategic partnerships with providers of services such as home security.

Some operators even consider other services such as telehealth and utilities (e.g., electricity).

Main takeaways

UK AltNets should consider the following changes to their go-to-market strategy to become more attractive to customers:

- complement their sales channels strategy with a direct presence on the high street for better customer engagement

- evolve their product portfolio by introducing 3P/4P bundles, mirroring the approach of successful European AltNet counterparts

AltNets in Europe have successfully implemented these actions with good results. We believe UK AltNets could implement them to improve their take-up rates.