Despite its rapid adoption, 5G has not yet delivered a true breakthrough, lacking a defining use case to translate its promise into revenue growth

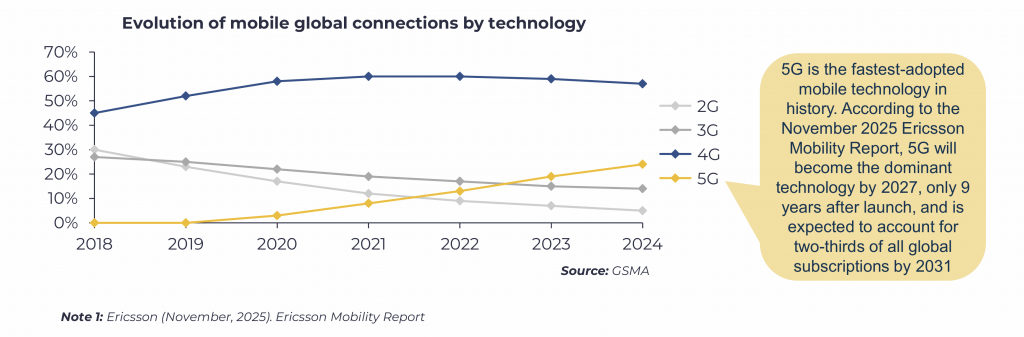

The evolution of mobile communications has been marked by decade-long generational shifts, from the voice-centric 2G era to the data revolution of 3G, and from the broadband surge enabled by 4G LTE to the advanced capabilities promised by 5G. Each transition has delivered higher speeds and greater societal impact. 5G emerged specifically to overcome the constraints of 4G networks: the need for ultra-low latency, massive device density, and the performance required for industrial automation, autonomous systems, and immersive digital experiences. As a result, the industry positioned 5G as the technological backbone of a hyperconnected society, integrating the worlds of telecommunications, cloud computing, and artificial intelligence.

The promise was compelling. Operators and governments viewed 5G as a strategic enabler of economic productivity, smart manufacturing and digital inclusion. For users, it was expected to unlock seamless virtual and augmented reality, intelligent transport and real-time entertainment. Thus, 5G deployment accelerated at an unprecedented pace. By the end of 2025, 5G subscriptions are expected to reach 2.9 billion, growing four times faster than 4G LTE during a comparable period1. Yet, this impressive adoption curve masks a profound paradox: widespread network roll-out has not translated into proportional financial returns for operators.

The pattern of generational adoption also reveals shrinking revenue cycles. Whereas 2G and 3G monetised voice and text with relative ease, 4G’s success relied on data traffic growth. In contrast, 5G lacks a distinct, mass-market “killer application” to drive incremental revenues. It has achieved technical maturity faster than any previous generation, but without an equivalent commercial breakthrough

5G’s rapid roll-out has strained operators financially, as rising investments surpass revenue gains, pushing the industry towards more efficient growth strategies

Behind the rapid roll-out lies an industry grappling with financial stress. Global operators’ capex related to building 5G infrastructure between 2023-2030 is expected to reach USD 1.3 trillion2. However, this investment surge has not been matched by revenue growth or higher ARPU. In many mature markets, telecom revenue has stagnated at low single-digit levels, often below inflation, while ROIC has fallen below the median WACC(less than7% by2024)3.

The traditional model, which assumed “build it and growth will follow”, has collapsed. Consumers display limited willingness to pay a premium for 5G, and operators have frequently bundled 5G access as a free upgrade, reinforcing the perception of it as “just another G”. This erodes any prospect of premium pricing and weakens the investment case.

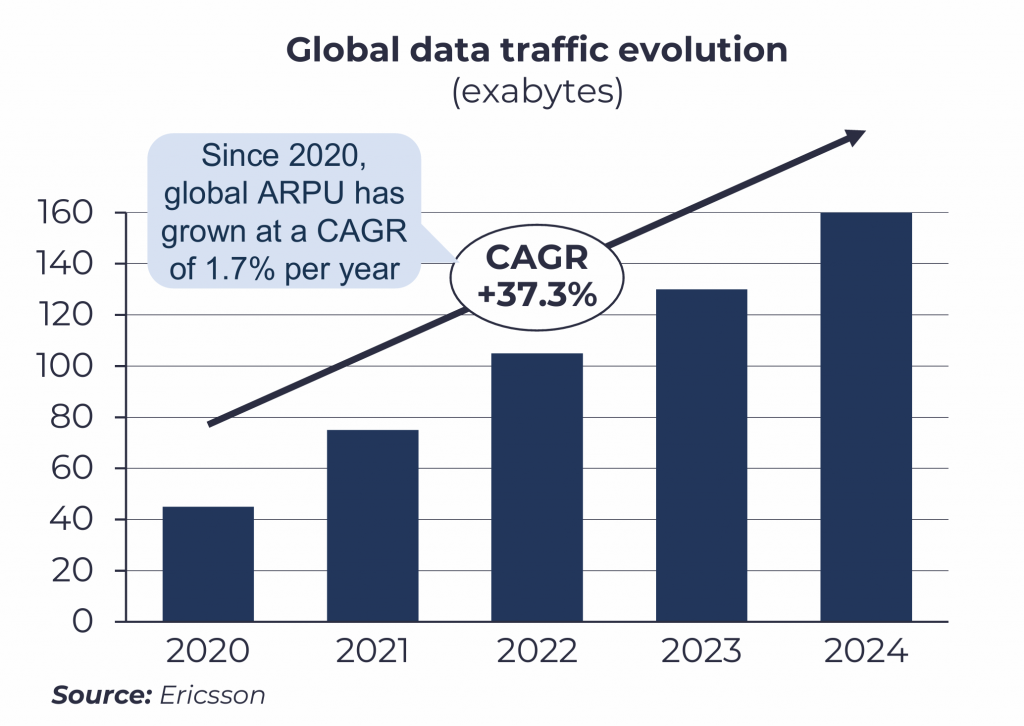

Meanwhile, subscriber and data use growth, the historical drivers of telecom expansion, are decelerating. The annual growth rate of 5G subscribers is expected to slow from 63% in 2024 to 21% by 20274, while traffic growth is forecast to grow by roughly 20% by 2028. These dynamics add uncertainty to the assumptions that initially supported operators’ investment frameworks.

Despite this deceleration, the latest Ericsson Mobility Report projects that 5G networks will carry around 83% of all mobile traffic by 2031. This highlights the intensifying pressure on operators to accommodate rising capacity demands while returns lag.

To address these pressures, the sector has entered 2024 a new phase of “smarter capex” instead of blanket coverage. Operators now apply AI-driven capital planning tools to target investments that maximise measurable improvements in user experience and revenue retention

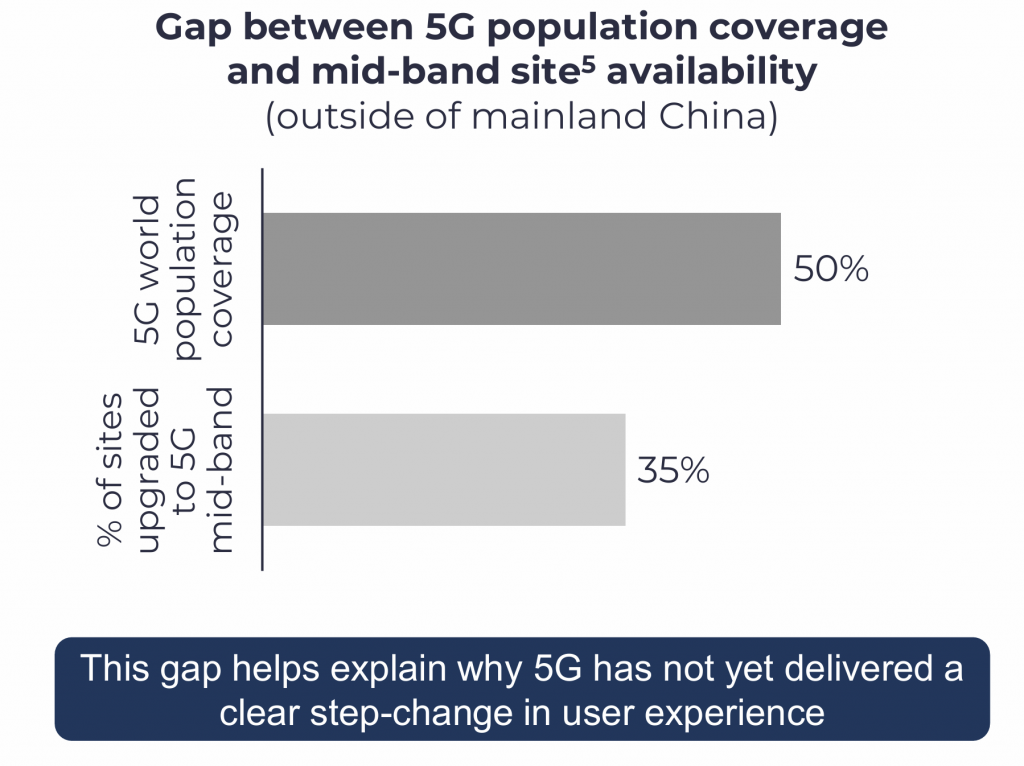

5G has yet to deliver a noticeably superior experience for the average customer

Faster speeds alone have not convinced users to pay more, particularly when many perceive 4G networks as sufficient for daily applications. This value-perception gap is the crux of the monetisation dilemma: if consumers cannot see tangible benefits, demand will remain muted, and without demand, operators will not invest further.

Note 2: GSMA. The spend of an era. mobile capex to reach USD1,5 trillion for 2023-2023. On-line:

https://www.gsmaintelligence.com/research/the-spend-of-an-era-mobile-capex-to-reach-1-5-trillion-for-2023-2030

Note 3: BCG. Returns May Be Declining, but Opportunity Is Calling. On-line: https://www.bcg.com/publications/2025/boosting-value creation-in-telcos

Note 4: GSMA. Unlock 5G Potential: How Intelligence Packet Core Drives 5G Monetization. On-line:https://www.gsma.com/get-involved/gsma-foundry/wp-content/uploads/2025/02/5G-Intelligent-Packet-Core-Whitepaper.pdf

Note 5: Mid band spectrum is the layer required for meaningful capacity and performance gains

With consumer monetisation constrained, the industry focus is shifting from selling data volumes to monetising the quality and nature of the user experience

The market has therefore entered a vicious cycle. Operators hesitate to deploy advanced “Standalone 5G” cores, which are required for features such as ultra-reliable low-latency communication and network slicing, because there is currently no tangible business case. Enterprises, conversely, delay investment in 5G-enabled systems until such networks exist. The result is a chicken-and-egg stalemate. Overcoming this impasse requires redefining the 5G value proposition around differentiated experiences rather than raw connectivity. Only by linking specific use cases such as gaming, high-definition streaming, telemedicine or industrial control to assured performance can operators create willingness to pay.

Recent data from the November 2025 Ericsson Mobility Report indicates significant but uneven progress: 118 documented slicing use cases are already in development, with 65 of them having been commercially launched. Nearly 45% of global slicing activity is concentrated in Europe, underscoring that 5G Standalone (SA) traction is materialising first in financially stronger markets.

The evolution of 5G SA will therefore be selective rather than universal. As a result, only markets with sufficient financial strength can justify a complete transition to a standalone core. Elsewhere, deployments will be surgical.

Currently, the industry is exploring a range of new strategies:

- Network APIs:A newer frontier involves exposing programmable network capabilities, such as latency control, location verification and security, to external developers through APIs. Initiatives like the GSMA Open Gateway aim to create common standards, turning the network into a platform for innovation, much like the internet did for software. The model remains nascent but could unlock recurring, service-based revenues if executed collaboratively.New API categories such as Quality on Demand (QoD), User Route Selection Policy (URSP), and early low-latency scheduling pilots with Singtel for cloud gaming demonstrate that programmable networks are moving beyond theory into commercially testable models.

- Consolidation and strategic M&A:Mounting financial pressures have made consolidation imperative. The rationale is no longer merely scale but synergy, i.e. optimising overlapping networks, rationalising IT systems and combining complementary strengths. Emerging deal archetypes include in-market mergers, infrastructure carve-outs, strategic divestments of non-core assets, and targeted bolt-on acquisitions for capabilities in cybersecurity, AI or software.

- Fixed Wireless Access (FWA): Using 5G to provide home and business broadband has become one of the most successful use cases. FWA offers operators a new revenue stream while helping bridge digital divides, particularly in underserved regions. In several markets, it accounts for up to a quarter of recent revenue growth.Ericsson projects that FWA will reach 350 million connections by 2031, with 90% of them through 5G, and will serve 1.4 billion people globally. This confirms FWA as the most mature and scalable 5G revenue driver to date.

- Private 5G networks:The enterprise segment represents the largest untapped opportunity. Private networks enable industries such as mining, logistics, healthcare and manufacturing to deploy secure, high-performance connectivity tailored to mission-critical operations. Yet, success requires operators to evolve from commodity connectivity sellers into integrated solution providers, with expertise spanning both information technology and operational technology.Recent deployments in Japan, Singapore and SailGP showcase real, commercial-grade slicing and deterministic performance for industrial automation and live event production, validating the enterprise value proposition of 5G SA.

We expect 5G monetisation to happen in three waves. First, the sustained expansion of FWA is already delivering measurable revenue gains. Second, differentiated QoE (via slicing, prioritisation and experience-based pricing) is expected to scale between 2025 and 2027. Third, a longer-term phase driven by AI workloads, Augmented Reality devices and enterprise automation, with uplink demand reshaping network economics.

Ultimately, 5G’s value will depend on clear monetisation logic, disciplined execution and coordination across the telecom ecosystem. The networks exist; the task now is converting connectivity into durable economic returns. 5G SA will not become universal in the near term. It is emerging as an ‘elite technology’, adopted first in financially stronger markets with defined enterprise needs.

5G SA will not become universal in the near term. It is emerging as an ‘elite technology’, adopted first in financially stronger markets with defined enterprise needs. Operators must therefore align SA, slicing, FWA and network APIs into a coherent, financially grounded strategy.

In this environment, Fide Partners can help investors by providing rigorous commercial and technical analysis to identify sustainable value within telecom assets. For operators, designing strategic roadmaps that align monetisation initiatives with realistic investment returns. And for policymakers, advising on spectrum and infrastructure frameworks that balance fiscal objectives with industry trends. In short, we are eager to help the industry turn 5G’s technical promise into tangible economic value, bridging innovation, investment and impact.