The depreciation trap: How the TCO is reshaping the capacity geography

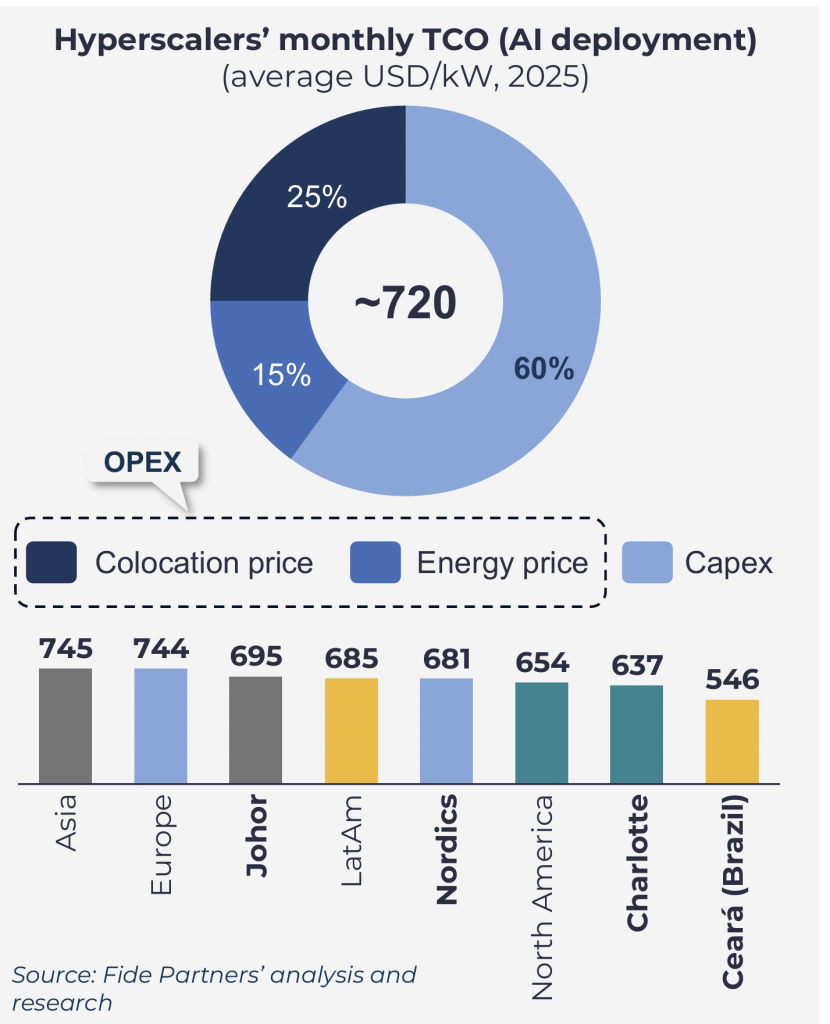

For hyperscalers, the economics of AI have introduced a brutal new variable: rapid hardware depreciation.

Unlike traditional infrastructure, where assets amortise over potentially decades, AI clusters rely on GPUs that cost hundreds of thousands of dollars but have 3- to 6-year obsolescence cycles.

This creates a “depreciation trap”. When recurring capex for server refreshes is this high, often dominating the TCO, the tolerance for inefficient opex diminishes. Operators simply cannot afford to pay premium power prices or punitive import duties (which can reach 40% of hardware costs) on top of massive, recurring hardware outlays.

Consequently, the market is shifting toward jurisdictions that can actively mitigate the cost basis through two mechanisms:

- Fiscal arbitrage: regions offering Free Trade Zone (FTZ) frameworks or fiscal exemptions that effectively subsidise the rapid refresh cycle.

- Energy arbitrage: markets with abundant and cheap renewable generation can decouple operating costs from the volatility of global energy markets.

For an industry that needs to replace its core assets every few years, these less saturated jurisdictions are where the depreciation curve and the power bill can coexist.

The geometry of latency: Strategic positioning in a connected world

Where will the next winners of the digital infrastructure race emerge?

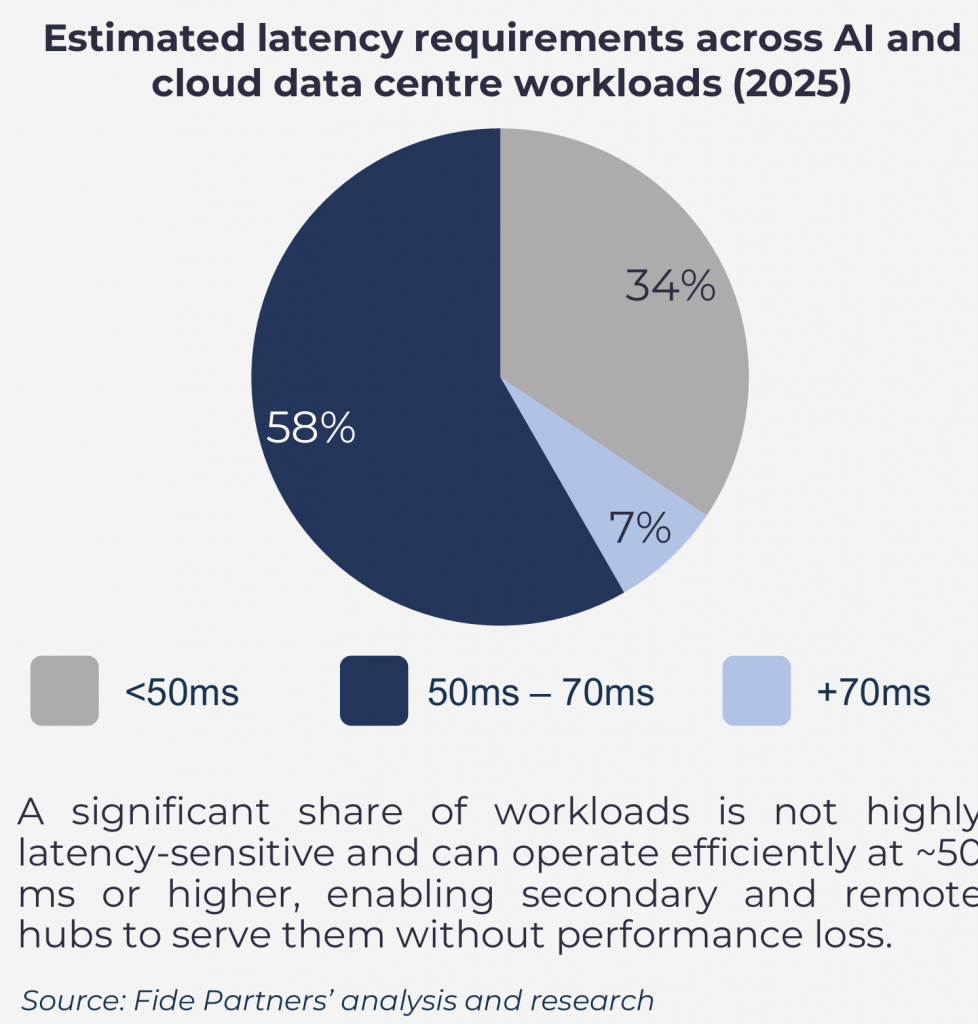

As digital demand continues to accelerate, TCO and connectivity have become two relevant forces actively reshaping hyperscale deployment logic. Power availability remains essential, but it no longer defines competitiveness on its own. Markets are rising in relevance when lower TCO, supported by fiscal incentives, FTZ frameworks, and renewable energy advantages, intersects with continental connectivity reach that enables the efficient servicing of workloads to important regions, even when these are not geographically adjacent.

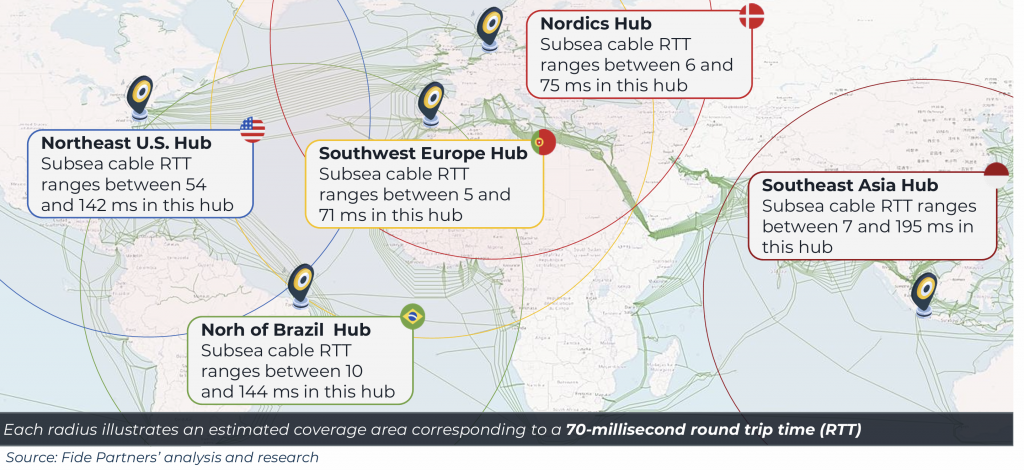

This convergence is already visible in regions where new cable landings amplify the impact of supportive policy. The upcoming Chile–Pacific connectivity corridor, for example, shows how a strategically positioned system might unlock intercontinental relevance when paired with competitive cost structures and pro-investment regimes. Similar dynamics are emerging across other markets that combine modern routes with hyperscaler-friendly economics, positioning themselves as credible alternatives for distributing global IT demand.

For operators, investors, and policymakers, the challenge is not only to identify where these dynamics are intensifying, but to act before the market fully internalizes their impact. The questions are who will recognize these inflexion points early and who will discover too late that the next major hub has taken shape in a place they once considered peripheral.